Market Commentary

For the first quarter of 2013 we look at three healthcare market segments, (i) healthcare services; (ii) diagnostic products and (iii) capital equipment used for pharmaceutical manufacturing and life sciences research. Significant companies in each segment include Baxter (NYSE: BAX), Thermo Fisher (NYSE: TMO) and Express Scripts (Nasdaq: ESRX), respectively.

Macro trends in healthcare affect these segments too; the first of note is the aging population in the U.S., Europe and other developed countries. The demand for healthcare products and services accelerates with age and also with wealth, whether the payment is direct, through insurers or government welfare programs. The second long-term trend is the increasing affluence of large segments of the population in China and India. Although country averages remain low, hundreds of millions of people in these Asian nations are now middle class and seeking quality healthcare. These two macro trends will, in the long term, support healthcare sector growth.

Recently growth in some economically-depressed markets has slowed; thus in southern Europe diagnostic test sales have softened in Greece, Portugal and Spain. These countries will continue to face challenges in managing public finances and meeting the needs of aging populations.

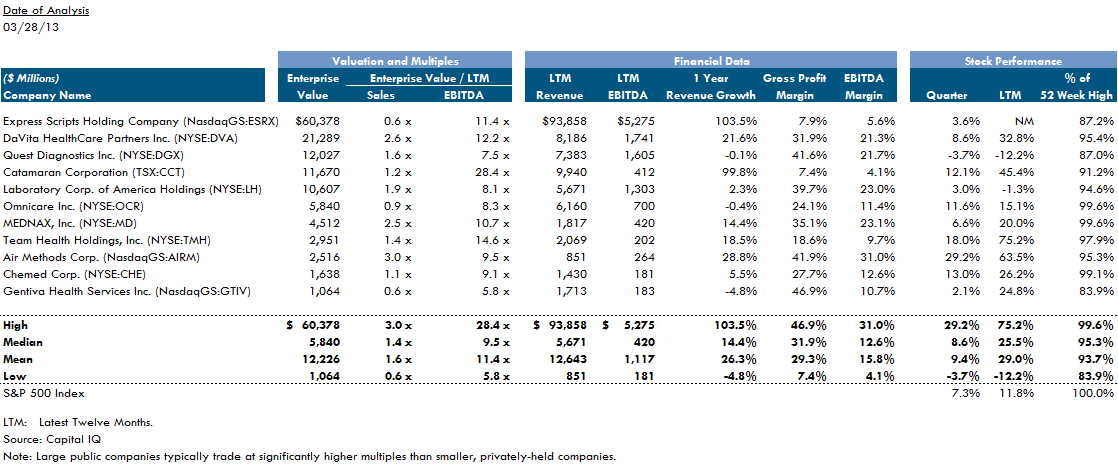

In the short-term, Medicare and Medicaid in the U.S. and other national healthcare authorities have exerted downward price pressure on pharmaceutical companies, hospitals and medical professionals (including the Healthcare Services segment). The overall effect is to narrow margins and provide incentives for more efficient and cost-effective solutions at all levels of healthcare enterprises. Median earnings margins in the Healthcare Services companies listed below have been 12.6% over the last 12 months.

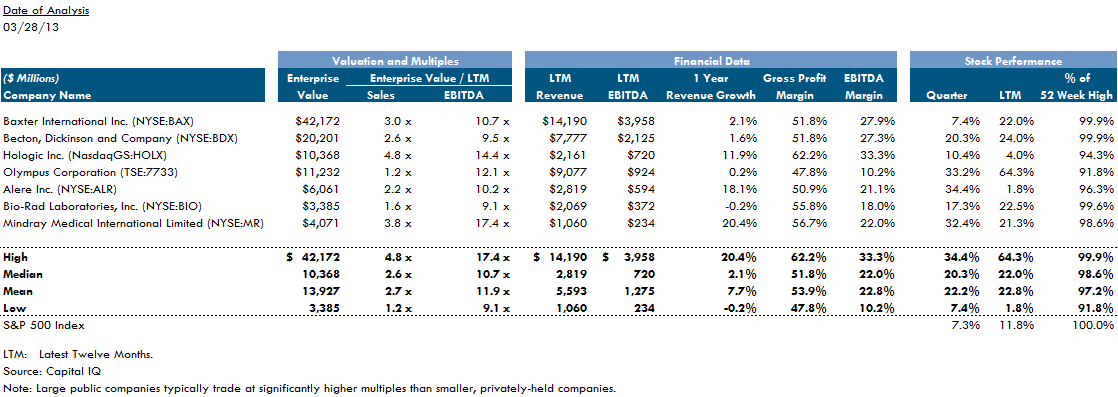

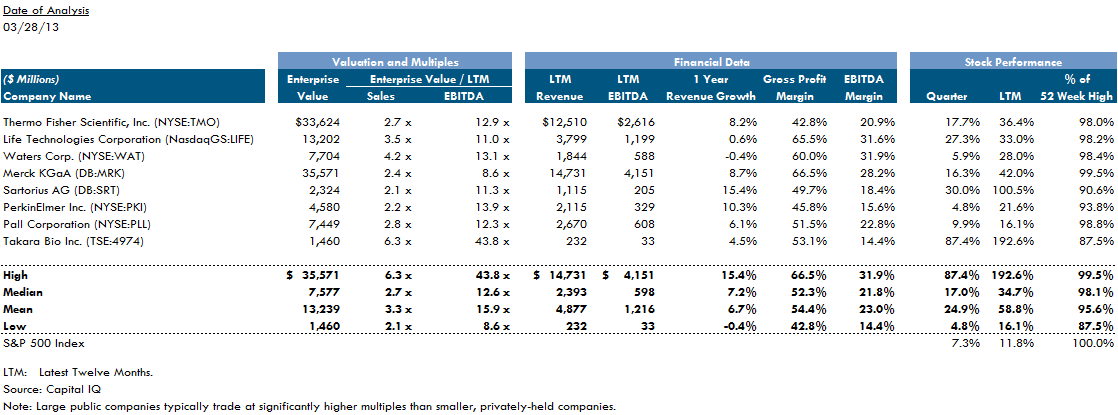

In contrast the earnings margins for diagnostic and biopharmaceutical equipment vendors are 22%. Among the salient differences are that these products are generally proprietary, that they are but a small part of the cost of treatment, manufacture or research, and in some cases these products reduce the overall cost of healthcare. For example, advanced bioreactors that increase the yields of therapeutic antibodies thereby reduce the risks and costs of manufacturing of advanced biopharmaceuticals; manufacturers are prepared to pay premium prices for technology that makes them more efficient. Similarly, advanced in vitro diagnostic tests can identify diseases earlier and permit intervention and therapy earlier, which in many cases results in better outcomes and lower costs.

Investors in these public companies appear to have recognized the log-term trends and are buying all three sectors with some exceptions. Median stock prices have grown twice as fast as the S&P 500 index in healthcare services and diagnostics; the real standout is the equipment sector, which has grown three times as fast as the S&P 500.

Public Comparables

Healthcare Services

Diagnostics

Biopharmaceutical & Life Sciences Equipment

Recent M&A Transactions

The buoyancy in biotechnology equipment stocks in the last twelve months may underpin the April 15, 2013, announcement by Thermo Fisher (NYSE: TMO) that it intends to pay $13 billion ($76 per share) for Life Technologies (Nasdaq: LIFE). Marc N. Casper, the president and chief executive officer of Thermo Fisher Scientific said “The acquisition of Life Technologies enhances all three elements of our growth strategy: technological innovation, a unique customer value proposition and expansion in emerging markets”. The importance of emerging markets is not lost on other buyers. George Barrett, the Chairman and Chief Executive Officer of Cardinal Health (NYSE: CAH) has said that it is that it is highly likely that they will continue to acquire in China. In the U.S. Cardinal is also focusing on the movement of care “away from the acute care centers towards the home and the ambulatory center”.

Of 58 transactions in the first quarter of 2013 Cardinal Health’s purchase of AssuraMed was the largest. On average, transactions were priced at 25.4 times revenues and 17.3 times earnings.

The 10 largest transactions in the last three months

Buyer | Target | Purchase Price (USD, millions) | Target Subsector |

|---|---|---|---|

Cardinal Health, Inc. (NYSE:CAH) | AssuraMed Holding, Inc. | 2,070.00 | Healthcare products distributor targeting the home market |

McKesson Corporation (NYSE:MCK) | PSS World Medical Inc. | 1,941.37 | Healthcare products distributor targeting physicians |

Health Care REIT, Inc. (NYSE:HCN) | Sunrise Senior Living Inc. | 1,468.71 | Assisted Living Facilities |

Allergan Inc. (NYSE:AGN) | MAP Pharmaceuticals, Inc. | 959.23 | Pharmaceuticals |

Illumina Inc. (NasdaqGS:ILMN) | Verinata Health, Inc. | 450.00 | Prenatal diagnostic tests |

The Medicines Company (NasdaqGS:MDCO) | Incline Therapeutics, Inc. | 390.00 | Drug delivery technology |

Wright Medical Group Inc. (NasdaqGS:WMGI) | BioMimetic Therapeutics Inc. | 376.97 | Replacement biomaterials for orthopedic surgery |

Linden LLC | Young Innovations Inc. | 320.46 | Dentistry products |

Cangene Corp. (TSX:CNJ) | Hemophilia Compound IB1001 and Related Assets | 300.00 | Pharmaceuticals |

Opko Health, Inc. (NYSE:OPK) | Proventiv Therapeutics, L.L.C. | 298.95 | Pharmaceuticals |

Research Team

Notice & Disclaimer

These materials were prepared by Westbury Group, LLC (“Westbury”), a broker-dealer registered with the Securities and Exchange Commission (“SEC” at www.sec.gov) and a member of the Financial Industry Regulatory (“FINRA” at www.finra.org) and the Securities Investor Protection Corporation (“SIPC” at www.sipc.org).

Westbury may act as investment banker to specific companies in the industry sectors described in this report by providing merger, acquisition, divestiture, private placement and other advisory services.

Westbury gathers its data from sources it considers reliable. However, it does not guarantee the accuracy or completeness of the information provided in this report. The material provided herein reflects information known to the authors at the time this report was written and such information is subject to change. Westbury makes no representations or warranties, expressed or implied, regarding the accuracy or completeness of this report.

Information, opinions and any estimates contained in this report reflect Westbury’s judgment as of the date written and are subject to change without notice. Westbury undertakes no obligation to notify any recipient of this report of any such change.

This report does not constitute advice or a recommendation, offer or solicitation with respect to the securities of any company discussed herein, is not intended to provide information upon which to base an investment decision, and should not be construed as such. Officers, directors, partners and employees of Westbury and its affiliates may have positions in the securities of the companies discussed, if any.

This report is not directed to, or intended for distribution to, any person in any jurisdiction where such distribution would be contrary to law or regulation.

Any public companies presented in this report are companies commonly used for industry information to show performance within a sector. They do not include all public companies that could be characterized within the identified sector and do not constitute recommendations for a particular security or sector. The charts, graphs and tables used in this report have been compiled by Westbury solely for the purposed of illustration.