Consumer

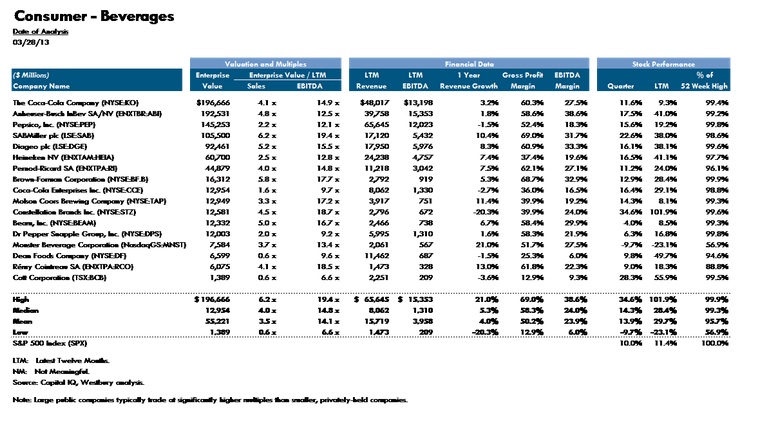

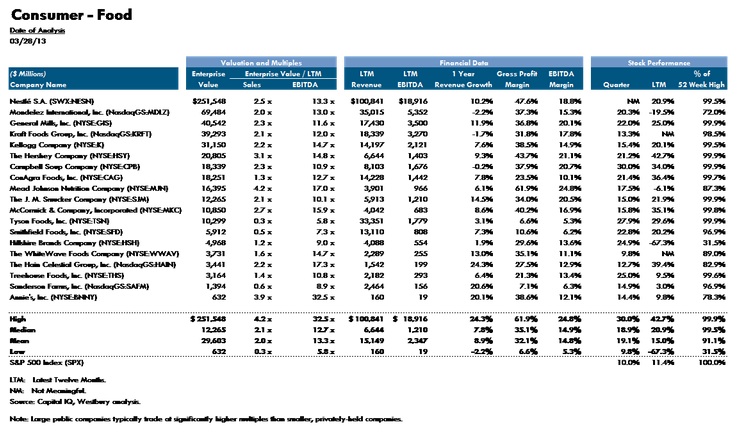

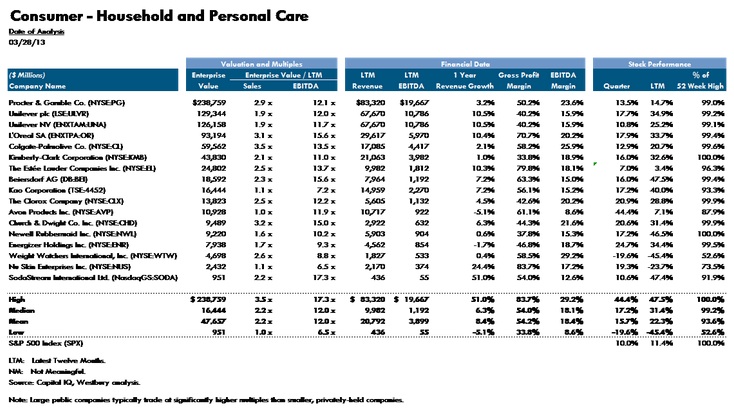

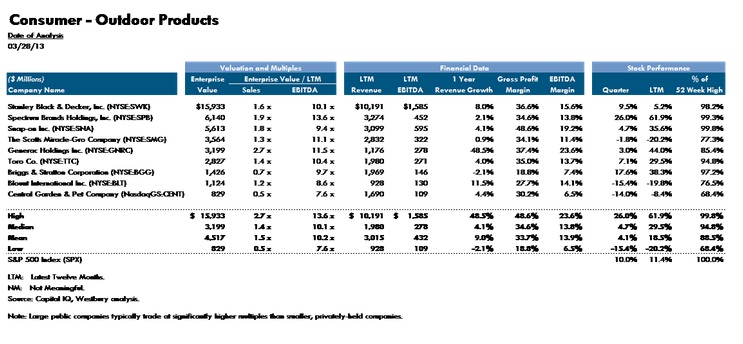

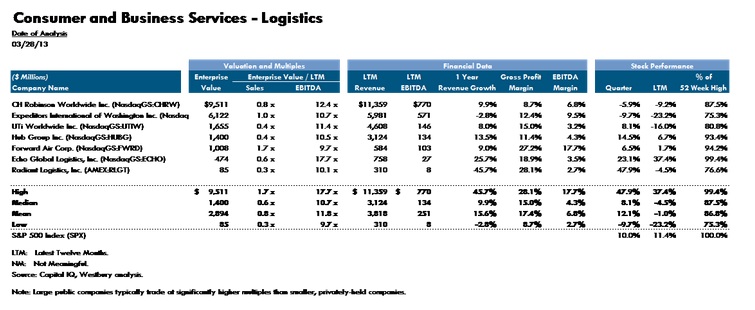

With roughly two-thirds of economic activity driven by consumer spending, the strength of the overall economy is dependent upon the health of the consumer sector. Non-discretionary consumer purchases remain robust: the year-over-year revenue growth of the Beverages, Food, and Household and Personal Care (HPC) sub-sectors exceeded the overall GDP growth. Furthermore, Westbury’s selected comparable companies within these sub-sectors outpaced the broader market. For example, the median revenue growth rates for Beverages, Food, and HPC were 5.3%, 7.8%, and 4.5%, respectively. Likewise, over the last twelve months ending March 28, 2013, these sub-sectors’ median stock price appreciation outperformed the broader market (as measured by the S&P500) by 17.6%, 10.5%, and 19.0%, respectively. Non-discretionary consumables such as gardening, home power generators, and lawn mowers have shown solid year-over-year revenue growth in excess of overall reported GDP growth. For example, the median year-over-year revenue improvement in Westbury’s Outdoor Products sub-category shows 4.1% growth. Over the last twelve months ending March 28, 2013, Westbury’s Outdoor Products median stock price appreciation outperformed the broader market (as measured by the S&P500) by 17.2%. Shipments of goods and the health of the logistics sub-category are also critical indicators of the economy’s direction. Westbury’s Logistics comparable companies demonstrate revenue growth over the past year with a median of 9.9% and the recent quarter’s stock performance (in-line with the broader market) suggest that there has been positive sentiment.

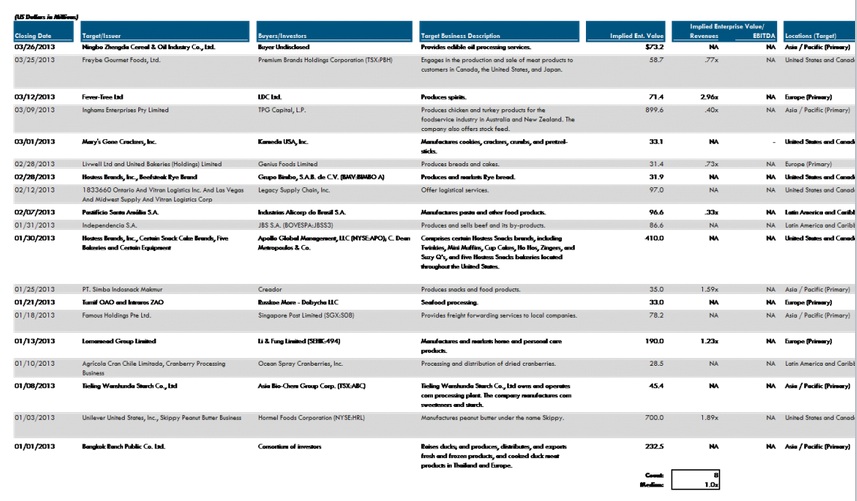

Selected Consumer Transactions

Retail

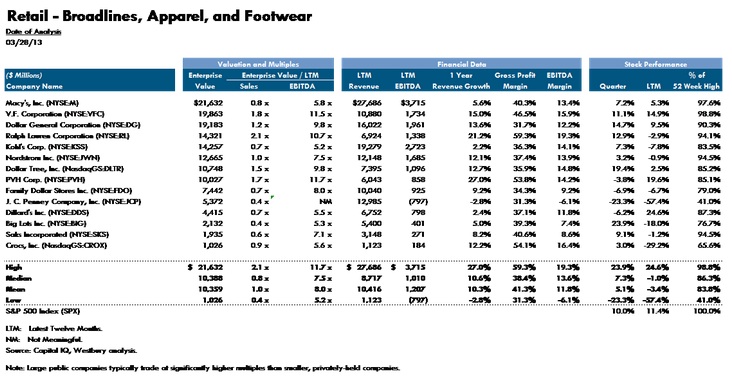

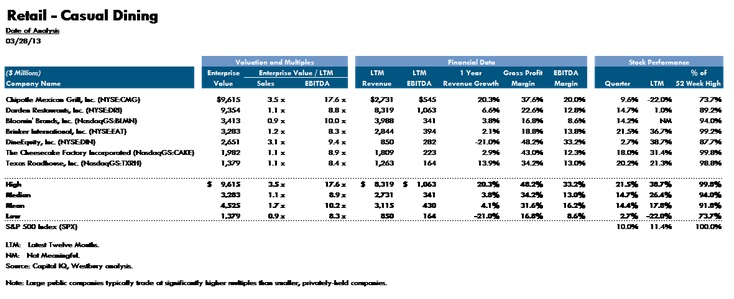

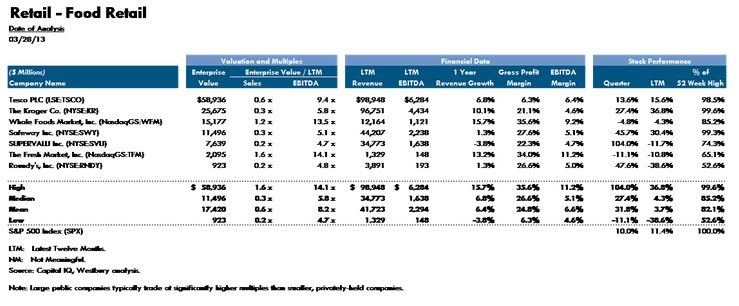

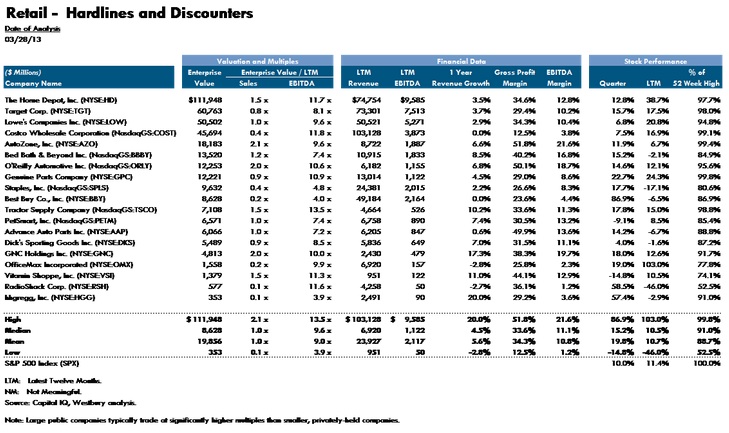

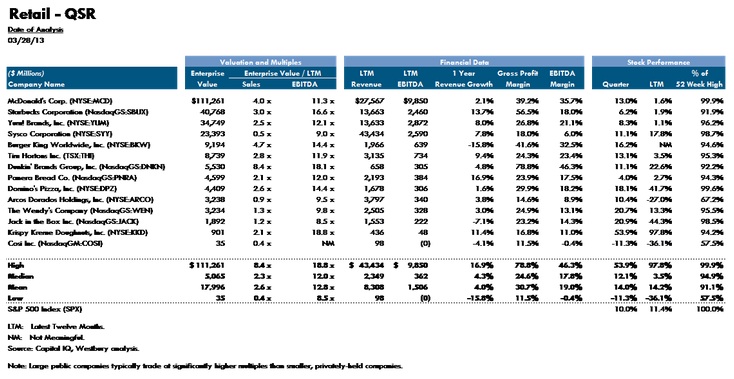

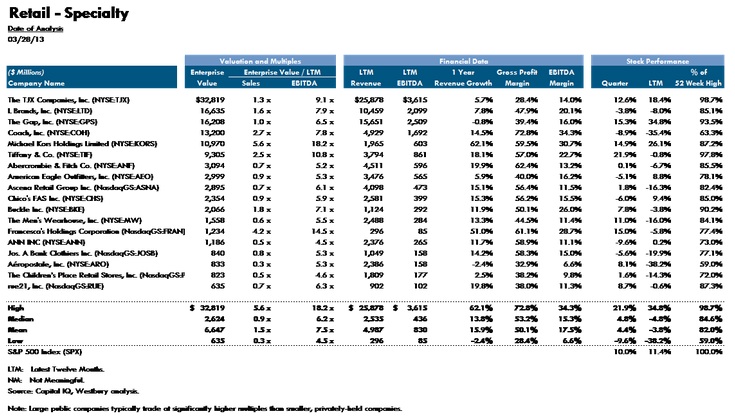

Coming off a challenging economic downturn, Westbury’s selected comparable Retail companies’ performance indicate that the consumer has been alive and well. The median one-year revenue growth rates for the Broadlines, Casual Dining, Food Retail, Hardlines and Discounters, Quick Service Restaurant (QSR), and Specialty are 10.6%, 3.8%, 6.8%, 4.5%, 4.3%, and 13.8%, respectively. Likewise, relative to the broader market (as measured by the S&P500), the retail sub-sectors have all outperformed the S&P500 during the last quarter ending March 28, 2013 except for the Specialty segment trailing by (2.5)%. Otherwise, Broadlines, Casual Dining, Food Retail, Hardlines and Discounters, and QSR exceeded the quarterly increase in the S&P500 by 0.5%, 6.5%, 18.4%, 6.7%, and 3.1%, respectively.

Selected Retail Transactions

Transaction Spotlight: Recent Significant Branded Consumer Food Acquisition

H.J. Heinz Company (NYSE: HNZ) (“Heinz” or the “Company”) announced on February 14, 2013 that it had entered into a definitive merger agreement to be acquired by an investment consortium comprised of Berkshire Hathaway and 3G Capital (the “Transaction”). Under the terms of the agreement, which has been unanimously approved by Heinz’s Board of Directors, Heinz shareholders will receive $72.50 in cash for each share of common stock they own, in a Transaction valued at approximately $28.7 billion, including the assumption of Heinz’s outstanding debt. The per share price represents a 20% premium to Heinz’s closing share price of $60.48 on February 13, 2013, a 19% premium to Heinz’s all-time high share price, a 23% premium to the 90-day average Heinz share price, and a 30% premium to the one-year average share price.

More than a decade ago, Heinz began a strategy of transforming itself from a U.S.-centric food company into a global one with a more focused portfolio of strong brands and favorable categories. With two-thirds of sales now generated outside of the United States and 25% of sales in emerging markets, the Company has built significant global reach and capabilities. Heinz is one of the world’s leading marketers and producers of healthy, convenient, and affordable foods specializing in ketchup, sauces, meals, soups, snacks, and infant nutrition. Heinz is a global family of leading branded products, including Heinz Ketchup, sauces, soups, beans, pasta, and infant foods (representing over one-third of Heinz’s total sales), Ore-Ida potato products, Weight Watchers Smart Ones entrées, T.G.I. Friday’s snacks, and Plasmon infant nutrition. Upon closing of the Transaction, Heinz will become a private enterprise and will remain headquartered in Pittsburgh, PA.

According to Bill Johnson, Company Chairman, President, and CEO, as noted from the related press conference on February 14th:

- The deal was offered at a 13.6x trailing EBITDA, 13.1x forward, and a 30% premium to the 10-year EBITDA trading average.

- At approximately $28.7 billion this will be the largest acquisition of any company in the history of the food industry.

- Since the buyers are considered primarily financial, anti-trust regulatory hurdles are considered minimal.

- The stock appreciation was 133% historically since 2006, and at the offer price, 177%.

- There are no financing contingencies to the Transaction.

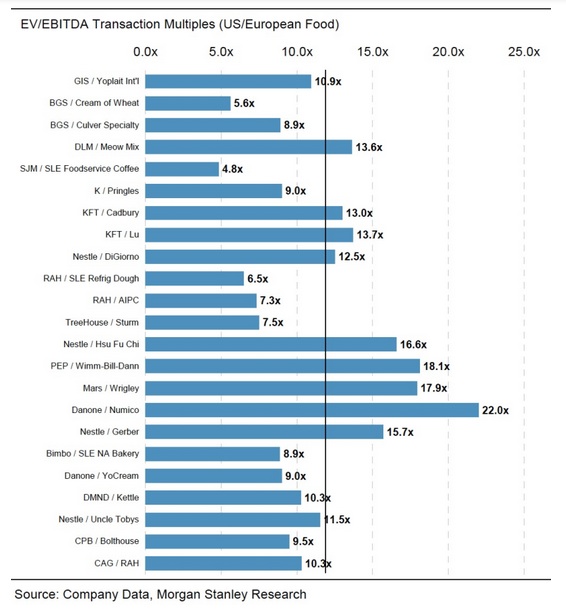

Trading at approximately 13.1x its forward EBITDA, the Transaction compares reasonably to other recent consumer branded food acquisitions:

There are few consumer branded food companies of the scope and geographic breadth of Heinz:

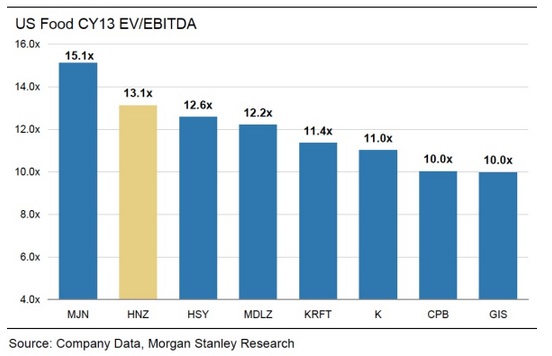

The Heinz acquisition announcement has been favorable for valuations in the sector as a whole, particularly the lower valued food enterprises:

Westbury would expect more transformational and large combinations to take place in the food sector on the tail of the Transaction, but not necessarily approaching the size of Heinz. Also, bolt-on acquisition opportunities of fast-growth, smaller food companies by the larger packaged food manufacturers is a theme we believe will be prevalent in this low interest rate environment.

Scott Silverman, Group Head

Patrick Huddie

Tim Williamson

Notice & Disclaimer

These materials were prepared by Westbury Group, LLC (“Westbury”), a broker-dealer registered with the Securities and Exchange Commission (“SEC” at www.sec.gov) and a member of the Financial Industry Regulatory (“FINRA” at www.finra.org) and the Securities Investor Protection Corporation (“SIPC” at www.sipc.org).

Westbury may act as investment banker to specific companies in the industry sectors described in this report by providing merger, acquisition, divestiture, private placement and other advisory services.

Westbury gathers its data from sources it considers reliable. However, it does not guarantee the accuracy or completeness of the information provided in this report. The material provided herein reflects information known to the authors at the time this report was written and such information is subject to change. Westbury makes no representations or warranties, expressed or implied, regarding the accuracy or completeness of this report.

Information, opinions and any estimates contained in this report reflect Westbury’s judgment as of the date written and are subject to change without notice. Westbury undertakes no obligation to notify any recipient of this report of any such change.

This report does not constitute advice or a recommendation, offer or solicitation with respect to the securities of any company discussed herein, is not intended to provide information upon which to base an investment decision, and should not be construed as such. Officers, directors, partners and employees of Westbury and its affiliates may have positions in the securities of the companies discussed, if any.

This report is not directed to, or intended for distribution to, any person in any jurisdiction where such distribution would be contrary to law or regulation.

Any public companies presented in this report are companies commonly used for industry information to show performance within a sector. They do not include all public companies that could be characterized within the identified sector and do not constitute recommendations for a particular security or sector. The charts, graphs and tables used in this report have been compiled by Westbury solely for the purposed of illustration.